Edge AI: A Second Chance for Japan?

Japanese IC vendors lost their way by sticking too long to in-house fabs, insisting on home-grown MCUs and tool sets. But rapid advancements in AI could nudge Japan toward embracing "buy" over "make."

In the semiconductor industry, “make-or-buy” decisions have had a “make-or-break” impact. Some companies hit the jackpot; others crapped out.

Among “make-or-buy” choices semiconductor companies have wrestled with are issues like staying with their own fabs vs. moving to fab light/ fabless, using open-source MCUs/CPUs vs. developing proprietary processing cores, and building internally developed electronic design automation tools vs. buying off-the-shelf tools.

Think Intel, Taiwan Semiconductor Manufacturing Co. (TSMC), AMD or Nvidia. They made choices that led them to where they are today.

Downfall of the Japanese semiconductor industry

Largely, in my view, Japanese vendors blew their make-or-buy decisions.

In a nation where “perseverance” is a prime virtue, and “giving up” on any project early is a disgrace, Japanese companies often make the wrong decisions at the wrong time. This usually comes down to a too-late pivot that leaves them trailing the competition.

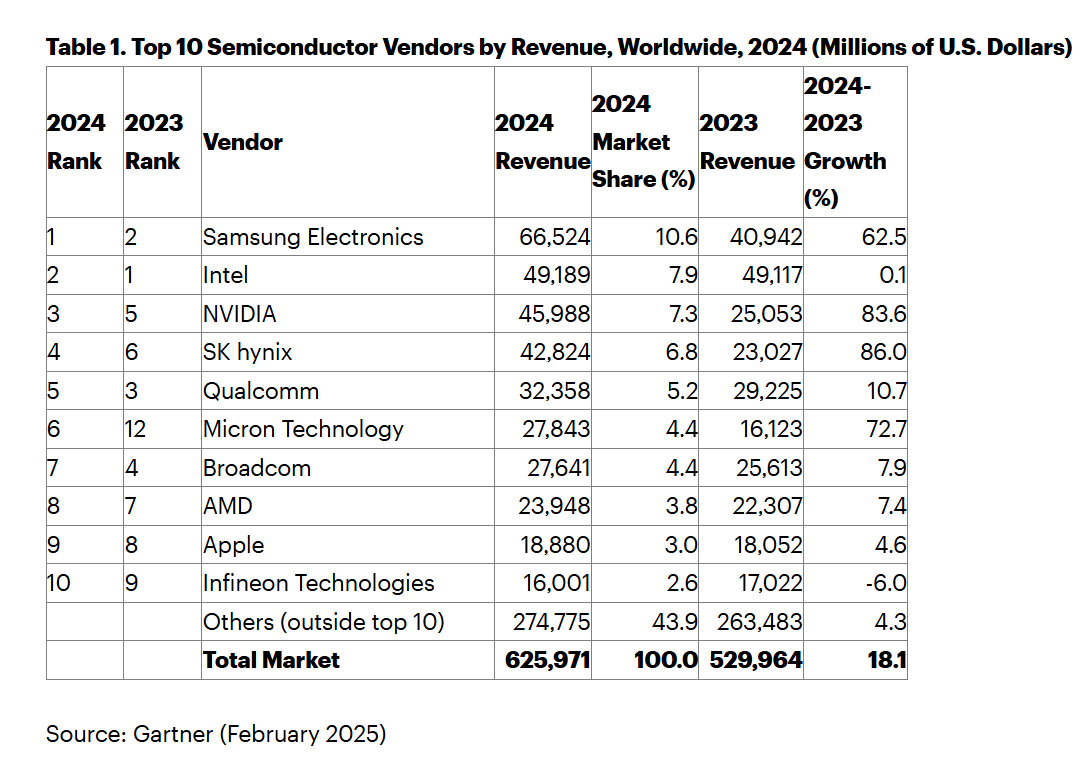

This tendency partly explains why no Japanese chip company ranks in the top ten of global semiconductor revenue. Compare this to 1989, when NEC, Toshiba, Hitachi, Fujitsu, Mitsubishi and Matsushita were among top ten chip vendors.

Jan Goodsell, vice president, business development-Japan, Quadric, agrees. Quadric is an AI inference IP company based in Burlingame, Calif.

Goodsell believes that one important factor that led to the decline of Japanese semiconductor companies was that “Japan unsuccessfully stuck with in-house fab model in the 1990s.”

Goodsell has held key executive positions in Japan working for U.S. IP, chip and tool companies. Looking back, he noted that big Japanese players, more than a few of decades ago, were planning foundries intended to compete with TSMC. But they “were unable to agree on a process/business model to merge their fabs.”

Goodsell said the Japanese companies focused too closely on proprietary processing cores. They squandered time and resources by “maintaining in-house processors (VR, SH, etc.).” Many were slow in moving to Arm, he added, “except Softbank,” who later became Arm’s eventual purchaser.

Further, Japanese semiconductor companies had “too little focus on Application-Specific Standard Parts (ASSP)-embedded software to differentiate” [their products]. While ASSPs took off on the global market, Japan missed the opportunity. Goodsell believes this led to Japan’s huge loss of business to Qualcomm, Nvidia and others.

As a cub reporter in Tokyo for the U.S.-based newspaper EE Times in the 1990s, I noticed other social and cultural factors at play.

I recall AMD’s founder Jerry Sanders once boasting that “real men have fabs,” and I saw similar “masculine” business philosophy motivating many Japanese organizations.

Japanese chip vendors were also steeped in a pride of “monozukuri” (meaning “production” or “doing it right”). They were adamant about manufacturing chips to perfection regardless of cost and time to market, regardless of what the market was really asking for. A case in point is Japanese DRAM makers. Asked to make memory chips for PCs, they insisted on manufacturing the same high-quality, long-lasting DRAMs developed for servers. Disregarding the concept of being “good enough,” Japanese chip companies lost the DRAM war to Samsung.

Japanese tech companies also suffered from the Not Invented Here (NIH) syndrome. For my first assignment in Tokyo, my New York editor wanted to know why Japanese semiconductor companies — Toshiba, Hitachi and NEC — kept developing their own EDA tools internally, instead of buying third-party off-the-shelf solutions.

What I found out: It took Japanese electronics companies too long to realize the colossal inefficiency of developing and maintaining home-grown tools while designing chips.

Build-or-buy decision by automakers

Fast forward to 2025.

Make-or-buy decisions are now encroaching on the automotive industry. Leading carmakers have been toying with the idea of developing their own “brain” chip, or a central compute processor for their future software-defined vehicles.

Their playbook is Tesla.

Tesla calls its system on a chip, FSD Chip, a “neural network accelerator” custom designed for Tesla AI processing.

In essence, that’s what many automakers — Honda, for example — say they hope to do.

This year, Honda and Renesas announced an agreement to develop a high-performance SoC for Software-Defined Vehicles.

Their mission, they said, is to “deliver industry-leading AI performance and power efficiency for Honda’s new electric vehicle (EV) series in the late 2020’s.”

Is Honda buying a system-on-a-chip from Renesas? Is Honda building its own AI accelerator?

The answer seems to be in the middle — or a hybrid. The companies hope to build a system that “utilizes multi-die chiplet technology to combine Renesas’ Gen 5 R-Car X5 SoC series with an AI accelerator optimized for AI software developed independently by Honda,” according to the press release.

It’s clear they are betting big on “chiplets” to create the flexibility and scalability necessary for next-generation software-defined vehicles.

The chiplet is a design concept, often described as a “Lego block” approach, that allows customers to snap together different chiplets from different manufacturers to build a custom SoC. However, the chiplets described by Honda/Renesas aren’t “Lego blocks” interoperable from different manufacturers. Theirs are custom chiplets built within their own ecosystem.

Chiplet: a ‘hybrid custom option’

This Honda-Renesas approach to custom chips is hardly new. Intel Fellow Jack Weast calls this approach “a hybrid custom option” that Intel has been offering to the Chinese automakers.

Weast, now based in Beijing, is vice president and general manager, Intel Automotive.

In our interview last fall, Weast explained that by using “an open chiplet-based architecture, an automaker or ecosystem provider can put their unique IP on a chiplet.”

OEMs also look for scalability.

The chiplet option emerged “because of challenges with monolithic dies. If you build a huge monolithic die that meets the high-end vehicle requirements, you just can’t scale that down from a cost standpoint,” explained Weast. “Automakers get frustrated because they need to use different solutions” for different levels of vehicles.

Using chiplets, however, “you take a monolithic design, you disaggregate it into its different parts,” enabling the CPU and GPU to be in different chiplets, he noted. “And then those chiplets can scale independently.”

Honda-Renesas chiplet plan

Neither Honda nor Renesas has yet to unveil details of their planned chiplets.

Goodsell, however, sees “a couple of paths” the companies can pursue.

One is to deploy a Renesas SoC for middle to lower-end vehicle models, adding chiplets around the SoC to create a high-performance compute processing capability, Goodsell suspects.

With so many sensors deployed in highly automated vehicles, Goodsell believes Honda wants to build 1,000 tops, 2,000 tops, 3,000 tops high-end computing for high-end cars. For that they will surround the SoC with chiplets, he explained.

The other path is for Honda to pursue differentiation in AI accelerators.

Honda, Goodsell mused, must be thinking that “we have our ideas, we have our algorithms, and we have smart people. We want to differentiate on the accelerator side.” While buying the main SoC from Renesas, Honda wants to differentiate by developing chiplets and embedding an AI accelerator.

Unknown now, however, is whether Honda plans to develop AI accelerators in hardware from scratch, or possibly licensing AI accelerator IP from third-party vendors like Quadric.

Second chance for Japan

The Japanese semiconductor industry’s remarkable 21st-century decline should have taught Japanese companies some important lessons.

First, Goodsell noted, “when you see the technology disruption, you need to move quickly.”

Second, he explained, “conservative resistance is not going to be a winning path … If you just keep the status quo and say, no, no, no, [insisting that] we are going to be better, you are unlikely to win.”

“Japan hands” like Goodsell are pulling for Japan to rise again. Can Rapidus, for example, fill the gap? Perhaps. Will Softbank’s acquisition of Arm do any good for Japanese electronics? Maybe.

Goodsell is betting on the rise of AI. AI models and algorithms are constantly changing and moving fast, issuing a wake-up call to Japan that could become a second chance.

Rather than clinging to the tradition of designing, developing and manufacturing in house, Japan can finally opt to pick the best IP and develop unique AI systems, while raising a new generation of engineers fluent in neural network algorithms.

AI’s rise creates “a chance for Japan to do something different and to move ahead,” said Goodsell.

Wishing for Japan’s resurgence might, of course, be pure romance. But Steve Roddy, CMO of Quadric, sees practical reasons to encourage Japan’s effort.

He noted, “you must understand how short the lifespan of the industry’s enthusiasm for the latest and greatest AI model is.” Whether it’s Llama, ChatGPT, Vision Language Model (VLM) or DeepSeek, a life cycle can be as short as three to four months, he said. In contrast, developing silicon takes ten times as long. “What we know of today as the hot, sexy algorithms aren’t going to be the ones people want to run in two and a half years from now, when chips are ready.”

It’s clear that Japan must shake its traditional NIH syndrome and rethink build-or- buy decisions.

Of course, Quadric has a vested interest in pitching its programmable AI inference core IP for Japanese companies to license. Quadric has already signed a development agreement with Denso, Japan’s leading tier one, for a Neural Processing Unit (NPU), a processor specialized for AI computation. Without naming names, Goodsell noted that several other companies are close to public announcements.

He added, “Putting Quadric’s business aside, I think Edge AI is the next chance” for Japan.

Among Japanese system companies including automotive and digital camera companies, although not many are left, “I see some really smart people are working on their AI strategy,” said Goodsell.

Even though I come from Japan, and my first job as a cub reporter was in Tokyo, it always bugged me why and how Japanese chip companies declined so rapidly. This is my attempt to explain it partly with the help of Jan Goodsell at Quadric.